EUDR, CSRD, CSDDD – Mandatory Regulations from an IBC perspective

Posted 2nd October 2025

Introduction

The European Union (EU) continues to lead with sustainability in terms of policy and practice and has been the primary political and legislative force with respects to Environmental, Social and Governance (ESG) issues across developed markets. Issues such as climate change, global biodiversity loss, human rights issues, and governance (non) transparency topics are all getting the full focus of the EU to address some of society’s most urgent concerns.

In 2020, the EU approved the Green Deal, and thereafter launched new directives and regulations, of which these include those important to nature specifically:

- The EU Deforestation Regulation (EUDR);

- Corporate Sustainability Reporting Directive (CSRD); and

- Corporate Sustainability Due Diligence Directive (CSDDD).

Our article discusses the most recent changes and updates the EU has made this year to its legal and regulatory instruments.

{kind=link}

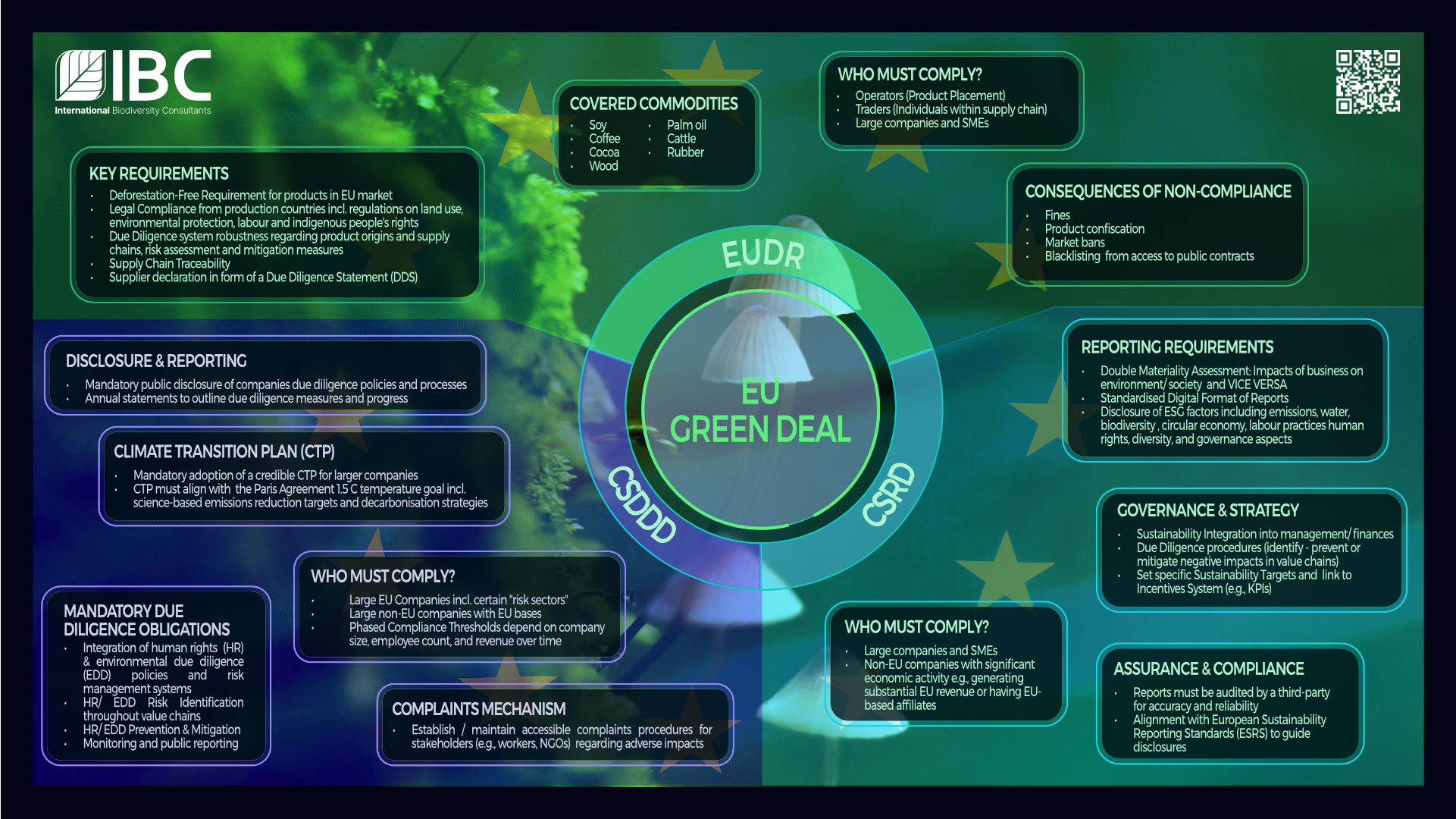

Figure 1. The European Green Deal.

EUDR

The EUDR focuses on deforestation and forest degradation linked products, including coffee, cocoa, soy, palm oil, beef, rubber, pulp, paper, and wood. These products can no longer be sold on the EU market without accurate due diligence; a legal and regulatory requirement that came into effect in December 2024/January 2025.

While the regulation should have been implemented in December 2024, the mandatory deforestation reporting was delayed by 12 months (to December 2025) for large and medium-sized companies; the reporting requirement for micro and small enterprises will be mandatory as of June 30, 2026. Delays were also caused by lobbying from third countries (e.g., naturally resource-rich countries that are heavily reliant on exporting forest products) and thus were concerned their home markets could be unfairly hit.

In late 2024, the EU launched the EUDR Information System for due diligence statements. Companies are now required to map their supply chains, gather geolocation data, and prepare for strict enforcement. Non-compliance of the EUDR may result in the goods being blocked from entering the EU market.

EUDR compliance is problematic for small and medium-sized enterprises in developing regions like those in Africa, South America and Southeast Asia. Whereas some of these regions enforce their own domestic regulations for anti-deforestation practices, as well as interrelated issues such as climate change, biodiversity loss, human rights, and good governance, these may not come up to the same standards as in Europe.

CSRD

The CSRD is aligned with the European Sustainability Reporting Standards (ESRS), in relation to ESG. The Directive has been discussed in length and has been under lobbying pressure since early 2025. Indeed, earlier this year, the EU delayed its reporting deadlines, calling it the ‘Stop-the-Clock Directive’ to give companies more time to prepare and adapt. In February 2025, simplification proposals were published under the heading of the ‘CSRD Omnibus Package’ which aims to reduce administrative burdens, thus making disclosure processes easier for companies. In July 2025, the European Financial Reporting Advisory Group (EFRAG), the body overseeing the ESRS, updated its draft standards, transforming it from highly prescriptive rules to more principles-based ones.

The issue is that although deadlines and rules are simplified, the demand for ESG data from investing and supply chain partners is still high. Therefore, companies cannot afford to waste time but need to prepare as quickly and as much as possible for what is to come. Indeed, many companies continue with their own set timelines in these regards, as postponement of actions is no longer an option. Additionally, small and medium-sized enterprises can voluntarily report on ESG items through the Voluntary SME (VSME) reporting standards.

CSDDD (2028 à)

The CSDDD is still in development as of the day of publishing this article. The Directive will require companies to identity, prevent, and mitigate adverse human rights and environmental impacts across operations and supply chains in detail. Implementation will start from 2028 for large companies and will be extended to 2029 for mid-sized firms. However, investors and buyers are already pressuring companies to adapt and implement these due diligence measures for reasons of transparency, reputation, and (future) compliance.

What does this all mean for companies?

Although these delays and simplifications may seem like companies have more time, combined these three regulations will create a compliance crunch between 2025 and 2027. A few aspects need to be highlighted here:

- Supply chain traceability is no longer optional;

- Sustainability reporting will become more stringent, similar to current mandatory financial reporting requirements; and

- Due diligence on both human rights and environmental issues will evolve from a voluntary to a mandatory requirement.

Forward looking businesses will use this time to invest in tools, build ESG reporting systems, and conduct early engagement with suppliers. This will give them a competitive market advantage, not only in terms of reporting on ESG topics, but also regarding trickle-down impacts on financial aspects of businesses. For instance, non-compliance will delay goods within the supply chain, causing losses in sales and revenues.

A final version of Omnibus 2 will be available by the end of 2025 or the beginning of 2026, and thereby the final versions of CSRD and CSDDD will hopefully be available by then.

Recently, uncertainty over the future of EUDR seems to have re-emerged, as the European Commission (EC) stated it must resolve certain IT issues first. This may delay reporting compliance by another year (to December 2026). In the advisory firms can also support companies with their due diligence statements in order to comply with the EUDR.

Other upcoming laws, regulations, and market approaches to be aware of:

EU Nature Restoration Law

The EU Nature Restoration Law focuses on the first EU wide binding legal framework for restoring degraded ecosystems amongst its members states. It came into force in August 2024 and aims to protect and restore 20% of land and 20% of the sea in Europe by 2030, with which the focus lies on climate and disaster mitigating ecosystems. This new law is related to other existing nature related policies and regulations such as Nature 2000, the Bird and Habitat Directive, and others. In addition, it is closely related to the United Nations Conference on Biological Diversity agreed with its Kunming – Montreal Global Biodiversity Framework (GBF) in January 2024 to protect 30% of land and 30% of sea by 2030.

EU Nature Credits

The EU launched a new roadmap on Nature Credits in June/July 2025, which aims to bridge the financial gap for nature restoration and conservation worth 700 billion USD annually on a global scale. Governments will need to provide 200 billion USD as of February 2025 (UN Biodiversity Conference of Parties), with the private sector required to contribute 500 billion USD, either as a stand-alone, or through blended finance (public-private), of which the latter is preferred.

How can IBC help?

At IBC we can help your company (large or small) with deciphering and meeting compliance for EU’s Nature Laws. We have team members located in the EU who can provide support and guidance. In addition, we can also help support if you are considering alignment with the Taskforce on Nature related Financial Disclosures (TNFD). IBC can also prepare Biodiversity Strategies and Finance plans in order to comply with these requirements of Global and Regional significance for nature, business and society. Use our contact form or email us at info @ ibioconsultants.com

About the Author

LAVINIA WARNARS MSC. (ENVIRONMENTAL SOCIOLOGY) PHD CANIDATE (BIODIVERSITY FINANCE, VU AMSTERDAM)

IBC ASSOCIATE CONSULTANT

Lavinia is an ecopreneur and consultant in areas of biodiversity business, policy, finance, and projects. She gained her knowledge and experience from a broad and in-depth educational background regarding sustainability, international development, business, and finance from universities based in Nijmegen, Cambridge, and Frankfurt.

From 2008 – 2014, she participated in transforming Ecuador into a post-oil economy and towards a sustainable and regenerative economic system. Since then, the focus of her work is on biodiversity protection, regeneration and expansion with a combination of analysis regarding risks, impact, and opportunities.

In September 2025, Lavinia started as a part time PhD candidate in Biodiversity Finance at the Free University of Amsterdam. The inspiration for this research was a recent trip she made visiting European nature parks from 2023 to 2025.

Sources

ABN AMRO (2025). CIRCL: CSRD Update. 27 June 2025. Amsterdam, The Netherlands.

Ernst & Young. (2025). EU Deforestation Regulation now postponed by 12 months. Retrieved on 22 September 2025, On: https://taxnews.ey.com/news/2025-0127-eu-deforestation-regulation-now-postponed-by-12-months?utm_source=chatgpt.com

- (2025). Simplification council agrees position on sustainability reporting and due diligence requirements to boost EU competitiveness. Retrieved on 22 September 2025, On: https://www.consilium.europa.eu/en/press/press-releases/2025/06/23/simplification-council-agrees-position-on-sustainability-reporting-and-due-diligence-requirements-to-boost-eu-competitiveness/?utm_source=chatgpt.com

EU Nature Restoration Law (2025). Nature Restoration Law enters force 2024. Retrieved on 22 September 2025 On: https://environment.ec.europa.eu/news/nature-restoration-law-enters-force-2024-08-15_en?utm_source=chatgpt.com

EUDR (2024). Deforestation Regulation Free Products. Retrieved on 22 September 2025, On: https://environment.ec.europa.eu/topics/forests/deforestation/regulation-deforestation-free-products_en?utm_source=chatgpt.com

Flammer, C., Giroux, T., and Heal, M.T. (2025). Biodiversity Finance. In: Journal of Financial Economics 164 (2025), 103987.

NBA. (2025). CSRD work congress. On 15 September 2025. Utrecht, The Netherlands.

PWC. (2025). The ESG Omnibus. Retrieved on 22 September 2025, On: https://www.pwc.nl/en/topics/sustainability/esg/sustainability-regulations/the-esg-omnibus.html?utm_source=chatgpt.com

VBDO. (2025). AGM engagement seminar. 26 June 2025. Amsterdam, The Netherlands.

United Nations. (2024). UNCBD / GBF. 10 January 2024. Retrieved on 29 September 2025: https://www.cbd.int/gbf